Commentary: Fifty-one cents on the dollar — the quiet fight over Lexington's police and fire pension

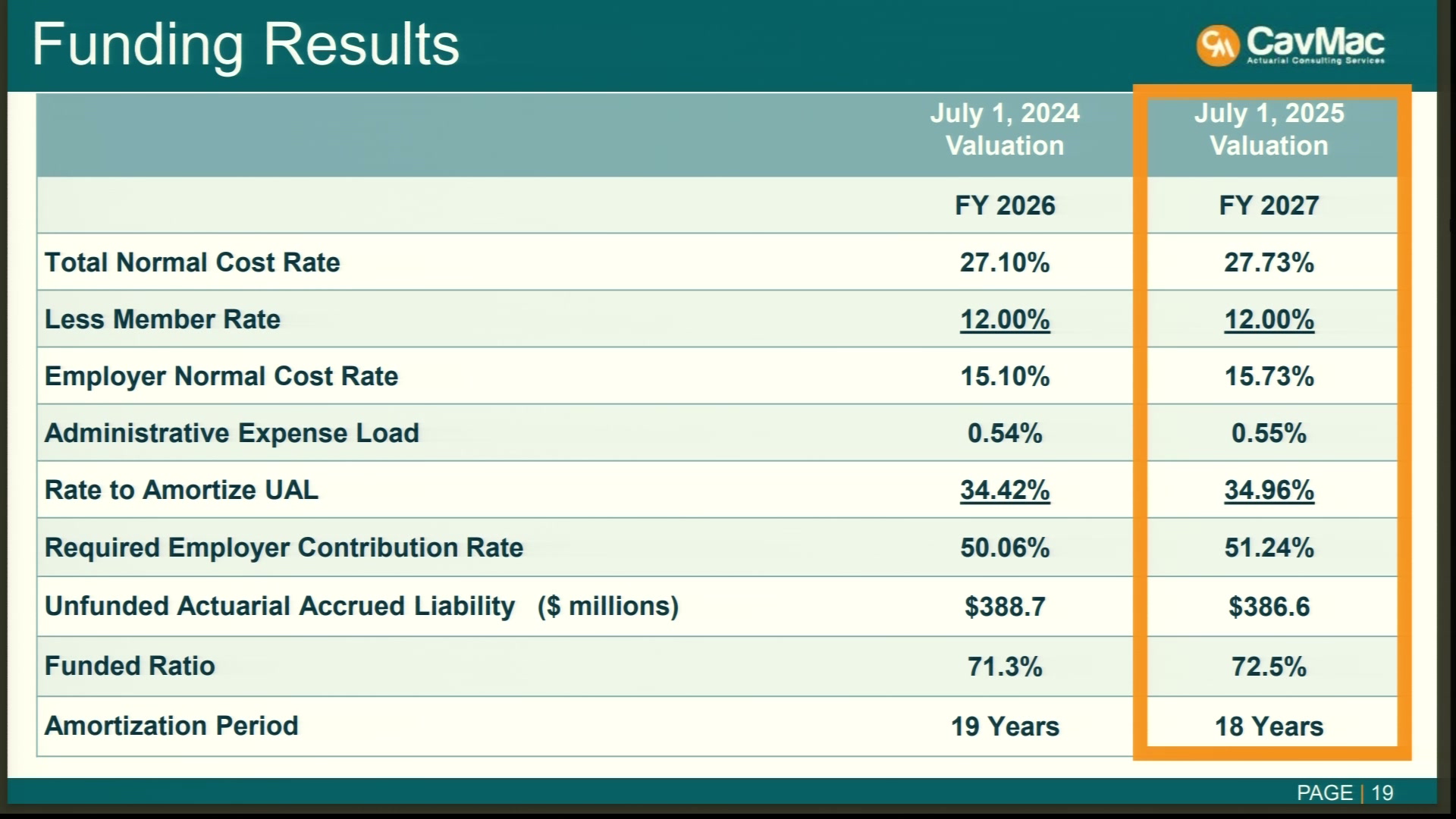

At nine o'clock on a Wednesday morning in January, in a meeting no reporter attended, the board of Lexington's Police and Fire Retirement Fund voted by voice vote to set the city's pension contribution at 51.24 percent of police and fire payroll.

Read that rate again. For every dollar Lexington pays a police officer or firefighter in the fiscal year that starts July 1, it will pay another 51 cents into the pension fund. In the budget the Urban County Council adopted this week, the line item comes to about $52.5 million — $25.4 million booked under police, $27 million under fire. One participant in the fund's October subcommittee meeting put it plainly: roughly 10 percent of the city's budget already goes to this one obligation.

Nobody covered the January vote. Nobody covered the October meeting. The last time any news outlet looked hard at this fund's finances, by our count, was 2018. The Lexington Times has been transcribing the meetings all along, and what sits in those transcripts is one of the most consequential — and most completely uncovered — fights in local government.

The last fund of its kind

Kentucky closed its city-run pension funds to new members in 1988 — every one of them except Lexington's. Because Lexington is the state's only urban-county government, its Police and Fire Retirement Fund operates under its own chapter of state law, KRS 67A.360 to 67A.690, and it still enrolls every new police officer and firefighter the city hires. Louisville's police are in the state's hazardous-duty plan. Lexington's are not, and never have been.

That independence has a price, and the actuary itemized it on January 14. Todd Green of Cavanaugh Macdonald Consulting — CavMac, on the slides — walked the board through the July 1, 2025 valuation: the fund holds just over $1 billion against roughly $1.4 billion in benefits already earned. The gap — the unfunded liability — is $386.6 million. The funded ratio is 72.5 percent, up from 71.3 percent the year before.

The slide the public never saw: CavMac's funding results, presented to the pension board Jan. 14, 2026. (LFUCG / Granicus)

An improvement, then. But zoom out and the picture stops improving. The fund was 72 percent funded in 2017. It is 72.5 percent funded now. Eight years of rising contributions and mostly good markets have moved the ratio half a point, while the dollar hole grew from $261.5 million to $386.6 million — 48 percent deeper.

The contribution rate climbed the same hill. In fiscal 2018 the city paid 35.8 percent of payroll, about $25.9 million. This coming year it pays 51.24 percent, about $52.5 million. Of that 51.24 points, only 15.73 cover the cost of benefits employees are currently earning. Another 0.55 covers administration. The remaining 34.96 points — two-thirds of the bill — is debt service on promises already made.

The retirees who eat the difference

While the city pays more, the people the fund exists for receive less, in real terms, every year. In 2013, with the fund in crisis, the General Assembly passed House Bill 430 at Lexington's request. Employees' own contribution went from 11 to 12 percent of pay. The city committed to a 30-year payoff schedule with a $20 million annual floor. And retirees' cost-of-living adjustments — previously 2 to 5 percent a year at the board's discretion — were cut to fixed tiers of 1, 1.5 or 2 percent.

Two retirees, police officer Tommy Puckett and firefighter Roger Vance Jr., sued, arguing the city had broken a contract. They lost. In August 2016 the Sixth Circuit ruled that retirees had no vested contractual right to the old COLA formula, leaving the General Assembly free to change it. And under the 2013 statute, the reduced tiers govern while the fund sits below 85 percent funded — a level it has never approached in the decade since.

The arithmetic of that ruling compounds monthly. At the January board meeting, a retiree rose during public comment and did the math out loud against the consumer price index, which had come in at 2.7 percent: 201 retirees get a 2 percent COLA, "so every single one of those lost 0.7." Another 880 get 1.5 percent. The 249 on the lowest tier get 1 percent — a loss of 1.7 points to inflation in a single year. "Our retirees are losing money every single month," he told the board, "and I hope that we can find some way in the future to help them." He noted he had made two motions in the fund's legislative subcommittee to do something about it. "Both went nowhere." Since that meeting, inflation has accelerated: the May 2026 CPI reading was 4.2 percent, a three-year high.

The quiet push to sweeten the deal

Here is where the story turns, because the pressure on this fund no longer runs only one direction. Through 2025 a Police and Fire Pension Subcommittee met at least six times — March, May, June (twice), July, October — to study making the pension more generous. The menu on the table in October: retirement after 20 years of service instead of 25, a benefit multiplier of 2.5 percent instead of 2.25, restored COLAs, and, on the fire side, a deferred-retirement program known as a DROP.

The motive is real. Lexington's police department was described in the June meeting as 129 sworn officers short — "we've never been 100 plus short for this period of time." Recruiters believe a 20-year pension is the carrot that fills academy classes. They are not inventing the idea: New York enacted exactly this in its 2025 state budget, cutting the NYPD's full-retirement threshold from 22 years back to 20 for officers hired after 2009, to fight a recruiting crisis of its own.

But every item on that menu adds to a liability the city already cannot seem to shrink. A board rule of thumb from the October meeting: each percentage point of COLA costs about a million dollars a year. A one-time "13th check" for retirees — floated as an alternative — would cost roughly $7.5 million, one month's retiree payroll. And the subcommittee's own survey of members came back inconclusive, with a slight lean toward the richer multiplier.

The meetings have not been gentle. The city's finance voice on the subcommittee, asked what would make him more comfortable with the actuarial projections, answered in two words: "Being trusted." He pointed out that the unfunded liability is "$120 million higher" than when the payoff plan started, despite the city paying $17 million a year more than it did three years ago. His metaphor for benefit enhancements: "If you continue to add to the ocean, you're never going to be able to get the unfunded liability paid off." He also disclosed a personal stake — his parents live off this fund.

The other side of the table answered with a line that deserves preservation: "Our funding ratio is great contrary to what anybody would believe. Having an unfunded liability does not make you a bad person."

There was an undercard, too: a fight over the police department's retiree-rehire program — "Officer R" in board shorthand — under which nine or so retired officers collect both pension and salary while neither they nor the city pay contributions on their new wages. "I hate our officer R program," one fire-side participant said flatly. The police side answered that the rehires were retiring anyway and the vacancies are real either way.

The honest counterargument

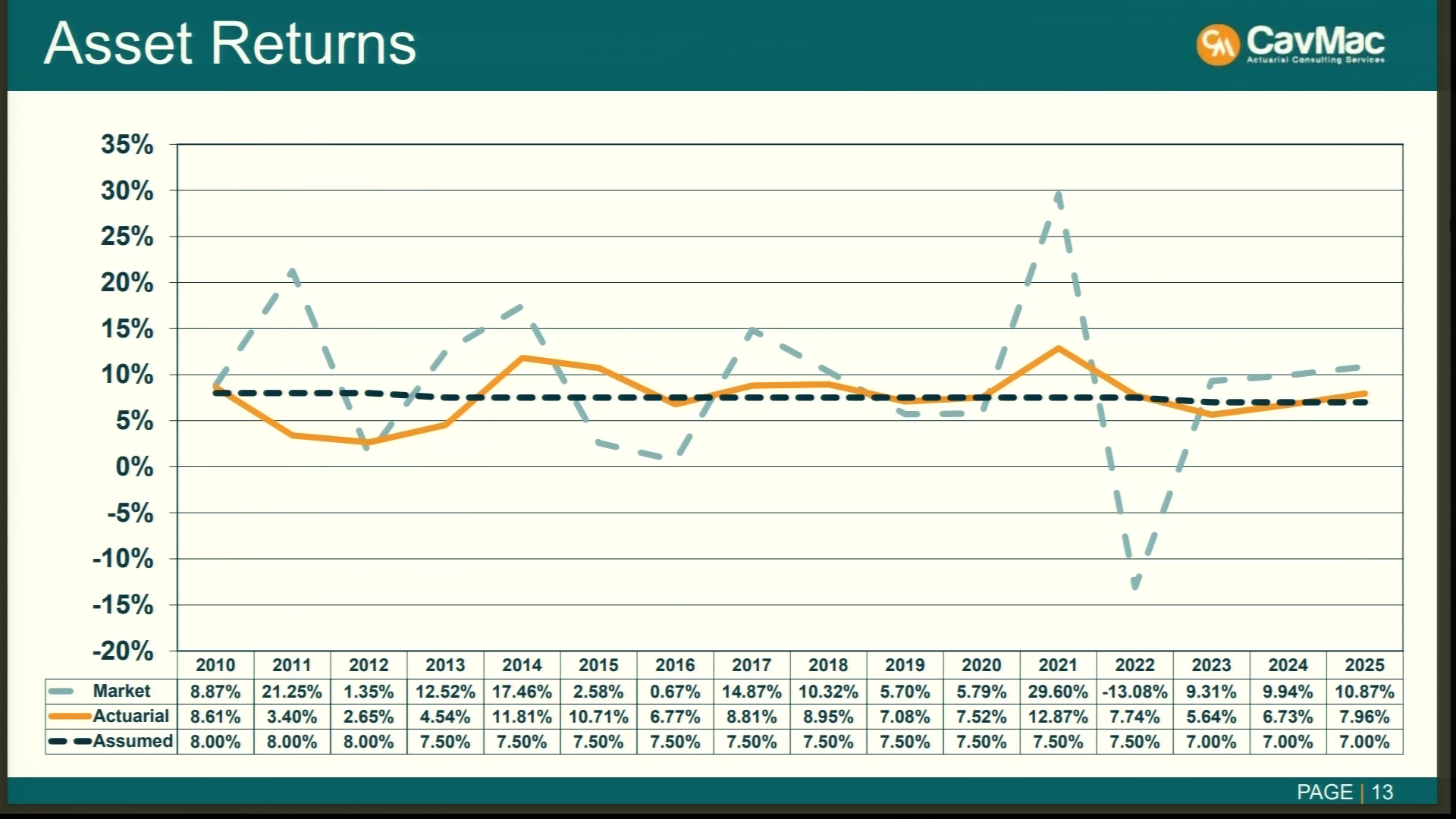

The fund's defenders have a better case than the raw numbers suggest, and it should be said plainly. Lexington's 72.5 percent funded ratio beats the statewide hazardous-duty plan that covers every other Kentucky city's police and firefighters — CERS Hazardous sits at 57 percent, with a $2.7 billion hole of its own. Much of Lexington's pain is self-imposed discipline: the 2013 deal put the debt on a closed 18-year countdown, like a mortgage with no refinancing, while the state plans amortize more gently. And the single biggest jump in the liability — roughly $118 million overnight in 2022 — came from the board lowering its assumed investment return to 7 percent. That made the hole look bigger because the old number had made it look smaller. Honesty is not mismanagement.

Sixteen years of returns: the 2022 crash (-13.08 percent) is still washing out of the fund's smoothed numbers; 2025 returned 10.87 percent against a 7 percent assumption. (LFUCG / Granicus)

The investments themselves are performing. The fund returned 10.87 percent in the valuation year and crossed $1 billion in assets. Sixteen million dollars in deferred gains land next year, then $12.4 million, then $7 million. If markets cooperate, the ratio finally starts climbing the way the 2013 reformers promised.

And the recruiting crisis is not imaginary. A pension that keeps officers in Lexington instead of losing them to departments with better terms has a value that never appears in an actuarial table.

What happens next, and who is watching

Every benefit in this fund is set in state statute. The subcommittee cannot change the multiplier, the retirement age or the COLA; it can only ask the General Assembly to. No Lexington pension bill appeared in the 2026 session, which adjourned in April — the October meeting's stated timeline was "We're looking at 2027." That means the next eighteen months are when the real decisions get made: which scenarios go to the actuary for pricing, what the city's lobbyist carries to Frankfort, what the Public Pension Oversight Board blesses.

All of that will be decided in meetings that, on present evidence, no one attends. There is a coda that says everything about how long this fight has run: the two retirees who sued the city in 2013 and lost now hold the board's two retiree seats. Tommy Puckett is the retired-police representative and runs the fund's continuation-of-benefits and legislative subcommittees, still pushing the retirees' case from the inside. Roger Vance holds the retired-fire seat. The city's finance office is still pushing back. Both sides are doing their jobs. The missing party is the public, whose $52.5 million a year this is.

Before any proposal leaves for Frankfort, three things should happen in the open. The actuary's pricing of every scenario under study — the 20-year retirement, the 2.5 multiplier, each COLA tier — should be published, not summarized. Any benefit increase should arrive paired with the funding source that pays for it, so the next generation of council members is not sitting where this one sits, wiring 51 cents of every payroll dollar into a hole dug decades earlier. And the question the retiree raised in January — whether the people who already served should keep losing ground to inflation while the city debates sweeteners for recruits — deserves a public hearing, not a voice vote at nine in the morning in an empty room.

The transcripts are public. The video is public. We will keep reading them. Someone has to.

Sources

- Police & Fire Pension Board, Jan. 14, 2026 — CavMac actuarial presentation of the July 1, 2025 valuation and the 51.24% rate vote (transcript + video)

- Police & Fire Pension Subcommittee, Oct. 27, 2025 — benefit-change menu, actuarial-trust dispute, Officer R debate (transcript + video)

- Police & Fire Pension Subcommittee, June 16, 2025 — unfunded-liability trajectory recitation, staffing shortfall (transcript + video)

- FY 2027 Mayor's Proposed Budget (adopted June 2026) — account 63513 Pension–Police/Fire: $25,433,469 (Police) + $27,047,761 (Fire)

- Puckett v. Lexington-Fayette Urban County Government, No. 15-6097 (6th Cir., Aug. 15, 2016) — COLA reductions upheld

- HB 430 (2013 Regular Session) — the Lexington police/fire pension reform act

- Kentucky League of Cities, Dec. 9, 2025 — CERS Board sets FY 2027 employer rates (hazardous 34.72%, hazardous plan 57% funded)

- CERS Actuarial Valuation as of June 30, 2025 (GRS for KPPA) — hazardous funded ratio 57.0%, UAAL $2.71B

- Public Plans Database, Lexington-Fayette County Police and Fire (plan 177)

- FireRescue1 / Lexington Herald-Leader, March 2018 — pension debt grows $77M (the 2017 valuation, last substantive press coverage)

- New York State Senate S2710 / A3968 (2025) — 20-year NYPD retirement for post-2009 hires, enacted via the 2025 New York state budget

- Center for Retirement Research, Boston College — the Dallas Police & Fire pension collapse (72% to ~35% funded)

- City of Lexington — Police and Fire Retirement Fund (board composition, governing statutes)