In its first year, Lexington asked the state for $973,179 in Red Mile tax money. Frankfort mailed $86,918.50. The subsidy's full ten-year ledger is now public.

→ Read the original on lexingtonky.news

On July 15 — the deadline it set for itself a month earlier — the Kentucky Department of Revenue delivered what it called its “final, supplemental response” to a Lexington Times open-records request: the increment letters, disbursement requests and internal calculation emails for the first five years of the Red Mile’s state tax subsidy, 2015 through 2019. Combined with the 2020–2024 records produced in June, the state-side money trail of the deal Lexington and the Commonwealth signed in 2011 is now public, end to end, for the first time. Kentucky law does not require these payouts to be published anywhere; the Kentucky Center for Economic Policy noted in 2018 that with state TIF deals “there is no way to know how much each project receives in incremental revenue payments each year.” Now, for one project, there is.

The complete ledger: $3.2 million in ten years

From 2015 through 2024 the state released $3,197,344.08 to the Red Mile Mixed-Use Redevelopment project — its share of new property, payroll-withholding and sales taxes generated inside the district, routed back to the development instead of the general fund. What Lexington asked for, and what Revenue’s auditors actually paid, year by year:

| Calendar year | City requested | State released | Difference |

|---|---|---|---|

| 2015 | $973,179.38 | $86,918.50 | −$886,260.88 |

| 2016 | $318,857.66 | $188,664.60 | −$130,193.06 |

| 2017 | $478,952.31 | $224,273.20 | −$254,679.11 |

| 2018 | $346,006.48 | $256,524.23 | −$89,482.25 |

| 2019 | $301,368.49 | $277,593.96 | −$23,774.53 |

| 2020 | $323,616.58 | $242,296.50 | −$81,320.08 |

| 2021 | $352,035.08 | $353,831.58 | +$1,796.50 |

| 2022 | $499,226.50 | $432,528.33 | −$66,698.17 |

| 2023 | $518,798.85 | $511,278.25 | −$7,520.60 |

| 2024 | $541,501.41 | $623,434.93 | +$81,933.52 |

| Total | $4,653,542.74 | $3,197,344.08 | −$1,456,198.66 |

Year one was the pattern

The 2015 request — Exhibit F, signed by then-Mayor Jim Gray — asked the state for $973,179.38. Most of it was a sales-tax claim built on $1,094,331.23 in reported receipts. When Revenue’s staff pulled the actual sales-tax filings from vendors inside the TIF footprint, they found $53,291.05 — about a twentieth of the claim — and even that had fallen below the inflation-adjusted 2009 baseline. The sales “increment” was negative: −$40,952.47, which the state offset against the rest of the subsidy. The submission had counted gross business receipts, sales tax paid on construction materials, and general business purchases; the statute counts only sales tax collected on sales made inside the footprint. Revenue’s first answer, in September 2016, was that the whole year netted out negative — no check at all. After the city sent more paperwork that October, the final answer came to $86,918.50. Lexington had asked for eleven times that.

The gamblers’ taxes

In an October 2016 email in the production, LFUCG’s finance office asked Revenue to add “withholdings from winnings in the Red Mile TIF in the amount of $19,609.00 for LTBA and $17,991 for KRM Wagering” — roughly $37,600 in income tax withheld from bettors’ winnings at the track’s new historical-horse-racing floor, submitted toward the subsidy as if it were payroll generated by the project. Revenue refused: withholding on gambling winnings “is not defined as new revenues within the grant agreement,” which counts only income taxes paid by employees of footprint businesses for work performed inside the footprint. The exclusion held. In a December 2018 internal email, Revenue tax policy analyst Jessica Martin described the working rule: “Any withholding reported on a W-2G for gambling winnings was excluded from the calculation.” (A W-2G is the IRS form reporting gambling payouts and any tax withheld from them.)

The same email records a second quiet correction: many W-2s filed under a single withholding account mixed wages earned at the Red Mile with wages earned at Keeneland, the track’s partner in the joint venture that runs the gaming floor. Revenue obtained a breakdown and struck the Keeneland-side wages from Lexington’s subsidy.

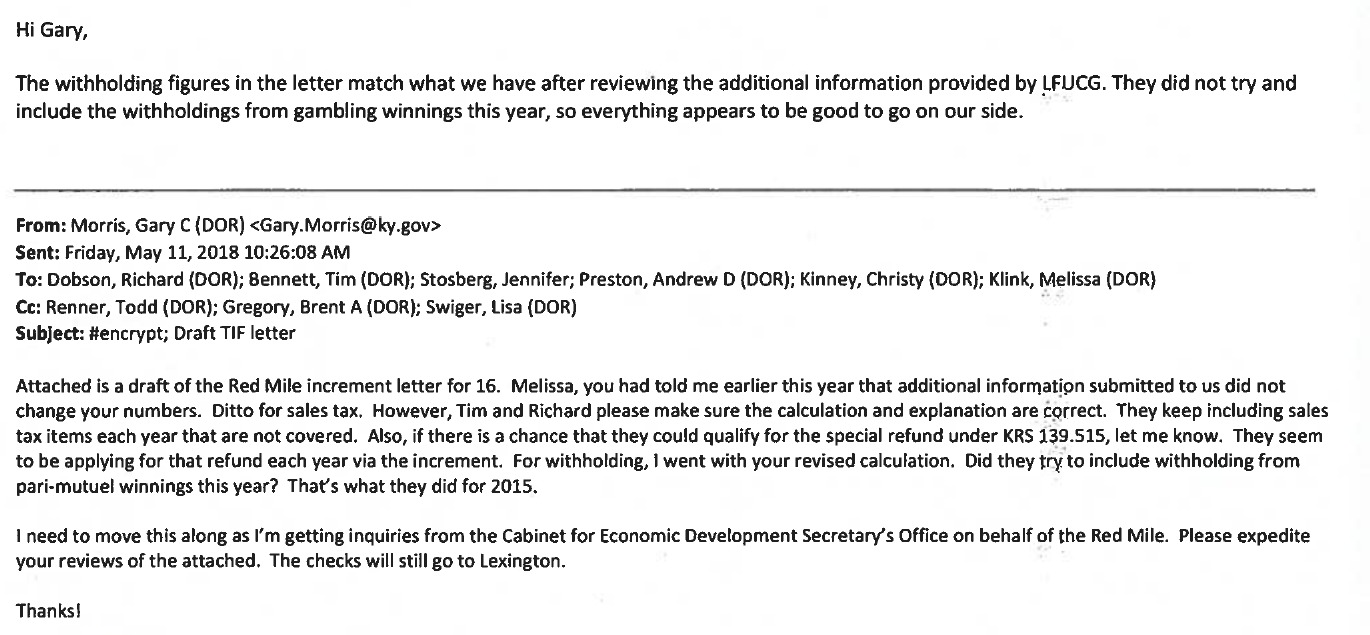

“That’s what they did for 2015”

By May 2018, the pattern had a shorthand inside the Revenue building. Reviewing the 2016 numbers, executive advisor Gary Morris asked his staff, in an email marked confidential: “Did they try to include withholding from pari-mutuel winnings this year? That’s what they did for 2015.” And: “They keep including sales tax items each year that are not covered.” A colleague, Andrew Preston, wrote back the all-clear: “They did not try and include the withholdings from gambling winnings this year, so everything appears to be good to go on our side.”

The same Morris email records where the pressure was coming from: “I need to move this along as I’m getting inquiries from the Cabinet for Economic Development Secretary’s Office on behalf of the Red Mile. Please expedite your reviews of the attached. The checks will still go to Lexington.” The cabinet that markets Kentucky’s incentive deals was leaning on the department that audits them — on behalf of the subsidized business.

A decade of corrections — in both directions

Every year from 2015 through 2024, Revenue recalculated what Lexington submitted. The cuts were for a recurring handful of sins, named in letter after letter: general business invoices — “similar to extraneous information your office provided the Department for both the 2015 and 2016 increment periods,” the 2017 letter says; vendors located outside the footprint, which took more than half off the 2018 sales claim; out-of-state “reciprocal” employees and out-of-footprint wages stripped from the W-2 data; and a 2017 property-tax increment claim of $223,830.93, built on $291,433.47 in claimed receipts where Revenue and the Fayette County Property Valuation Administrator found $53,204.26 — the state allowed $33,049.10, about a seventh of the ask.

But the record cuts both ways, and that is worth saying plainly. Of the gross $1.54 million Revenue struck from ten years of requests, about $1.08 million traces to two category errors: the 2015 sales claim built on gross receipts instead of taxable sales (about $842,000 of that year’s $886,000 cut) and the 2017 property line. The remaining roughly $460,000 was the substantive policing — out-of-footprint vendors, out-of-state employees, gamblers’ winnings. And in two years Revenue went the other way, adding back about $84,000: it bumped 2015’s property increment above the request, paid 2017’s withholding higher than Lexington asked, and — under the 2023 “phantom rate” law this newspaper reported in June — grossed the 2024 payout $81,933.52 above the request. Net, over ten years: $1.46 million less than Lexington asked. This is what a referee looks like. The question the record raises is not whether the state checked the math. It is why nobody in Lexington appears to have done so before mailing it to Frankfort.

The state’s own paperwork wobbled too

The production has its clerical moments. Revenue’s 2016 “final” letter stated a total that was a stale preliminary estimate; two weeks later Morris sent LFUCG a one-paragraph apology (“The Department of Revenue inadvertently included the initial increment estimate in our final letter”). The itemized amounts the letter directed checks for were correct — the summary sentence was not. The 2019 final letter repeats the trick, declaring “the total increment for 2019… is $256,524.23” — verbatim the 2018 total — while its own itemized breakdown sums to $277,593.96. And Revenue’s February 2020 letter records that the 2017 property-tax check “had not yet been issued” until January 6, 2020 — more than six months after the 2017 final letter, and nearly a year after its preliminary — when it was mailed alongside a 2018 check that went out prematurely. None of it appears to have changed what was paid. All of it is visible only because the letters are now public.

The question two agencies still will not answer

The deal’s foundational contingency remains unresolved on paper. The 2011 agreement set two caps on state participation: $25,321,000 if “instant racing” — historical horse racing — stood as a legal activity, $13,786,000 if it did not. The Kentucky Supreme Court held in September 2020 that the machines as then operated were not legal pari-mutuel wagering; the General Assembly legalized them by statute in February 2021. So which cap governs now? The Cabinet for Economic Development produced no analysis in June. Revenue answered the same question by sending the increment letters and pointing back to the Cabinet. On the evening of July 15, Revenue’s open-records counsel told The Lexington Times the question would be put to department staff. No answer has arrived. This article will be updated when it does.

Why the cap may not matter — and the calendar does

Here is the arithmetic that question runs into. Ten years of the twenty-year term have consumed $3,197,344.08 — 23.2 percent of the smaller cap, 12.6 percent of the larger one. For even the low cap to bind before the term ends in 2035, the remaining $10,588,655.92 would have to go out at an average of about $1.06 million a year — 1.7 times the biggest year the project has ever had, more than triple its ten-year average, starting immediately. At anything like the current pace, the lifetime total lands in the neighborhood of $10 million. The practical ceiling on the Red Mile deal is not either negotiated cap. It is the clock.

For scale: Kentucky’s historical-horse-racing machines took in $9.6 billion in wagers in fiscal 2024, producing $872.4 million in gross gaming win statewide, according to Kentucky Horse Racing Commission data. The 902-terminal gaming floor at the Red Mile — operated by KRM Wagering, the Red Mile–Keeneland joint venture entity inside the footprint, whose payroll drives roughly six of every ten dollars of this TIF’s withholding stream, per payroll backup in the Cabinet’s production — opened in September 2015, the same year the subsidy activated. The subsidy the state has policed line by line for a decade averages about $320,000 a year.

The complete open-records file — all three productions: the Cabinet for Economic Development’s June 12 response, including the 2011 agreement and its dual cap; Revenue’s June 22 production covering 2020–2024; and Revenue’s July 15 supplemental production covering 2015–2019 — is posted with this article, browsable by document, with a download-everything zip.

Sources

- Kentucky Department of Revenue — open-records response O-26-52R, supplemental production (July 15, 2026): Red Mile TIF increment letters, Exhibit F requests, and internal calculation emails, calendar years 2015–2019 (hosted with this article)

- Kentucky Department of Revenue — open-records response O-26-52R (June 22, 2026): increment letters and disbursement requests, calendar years 2020–2025

- Kentucky Cabinet for Economic Development — open-records production (June 12, 2026): KEDFA Tax Incentive Agreement (Aug. 25, 2011) with dual incentive cap ($25,321,000 / $13,786,000), amendments, activation records, and KRM Wagering payroll backup

- Kentucky Cabinet for Economic Development — TIF Projects with State Participation (Red Mile: activation Aug. 25, 2015; 20-year term; eligible incentive $13,786,000; estimated project costs $186,891,071)

- Kentucky Center for Economic Policy — "TIF Creep Means Growing Costs, Less Accountability" (year-by-year state TIF payouts not required by law to be made public)

- Family Trust Foundation of Kentucky, Inc. v. Kentucky Horse Racing Commission — Kentucky Supreme Court (Sept. 24, 2020): historical horse racing machines not pari-mutuel wagering

- Kentucky Senate Bill 120 (2021 R.S.) — redefined pari-mutuel wagering to include historical horse racing; signed Feb. 22, 2021

- Kentucky House Bill 360 (2023 R.S.) — "modified new revenues" income-tax gross-up for TIF projects approved before Jan. 1, 2023 (KRS 154.30-010)

- IRS — About Form W-2G, Certain Gambling Winnings

- BloodHorse — Red Mile–Keeneland joint venture opens 902-terminal historical-racing facility (September 2015)

- Hoptown Chronicle (Kentucky Horse Racing Commission data) — FY2024 historical horse racing handle $9.6 billion, gross win $872.4 million

- The Lexington Times — "Lexington just made the Red Mile's tax deal bigger" (June 5, 2026) and the 2020–2024 payout reveal (June 26, 2026), the investigations this report completes